More On: Bitcoin

How much 6 popular cryptocurrencies lost in 2022 ?

How people who watch the market were wrong about bitcoin in 2022

Twitter Is Too Musk to Fail

Why Jim Cramer suggests purchasing bitcoin or ethereum, with one exception

El Salvador's bitcoin experiment has cost $375 million so far and lost $60 million

The Fed's unprecedented monetary expansion has created damage that it cannot undo by switching directions.

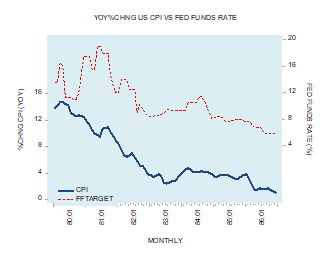

The Federal Reserve System of the United States lifted the goal for the federal funds rate by 0.25 percent on Wednesday, March 16, 2022, to 0.50 percent. According to Fed officials, the rise in the federal funds rate goal was prompted by high increases in the yearly growth rate of the Consumer Price Index (CPI), which stood at 7.9 percent in February compared to 7.5 percent in January and 1.7 percent in February of the previous year.

Most analysts believe that by boosting the interest rate target, the central bank will be able to slow the rise in the price of goods and services. Supporters of this method frequently point to May 1981, when then-Fed Chairman Paul Volcker hiked the fed funds rate goal from 11.25 percent in May 1980 to 19 percent in May 1981. The CPI's annual growth rate declined from 14.8 percent in April 1980 to 1.1 percent in December 1986. (see chart).

Figure 1: CPI vs. Federal Funds Rate

It is worth noting that critics refer to the CPI growth rate as inflation. However, we believe that increases in the money supply are what cause inflation. Furthermore, we do not claim that increases in the money supply produce inflation, as some critics argue. Instead, we believe that inflation is caused by increases in the money supply.

A good's price is the amount of money paid for it, but if there is an increase in the amount of money pumped into a particular products market, the price of the goods in money terms rises. This price increase, however, is not inflation, but rather the manifestation of inflation as a result of an increase in the money supply, all else being equal.

The harm inflation brings to the wealth-creation process is greater than the price rises it creates in retail items. This is deduced from the fact that increases in the money supply cause an exchange of something for nothing, resulting in a similar consequence to counterfeit money moving through the economy. It diminishes wealth generators, reducing their ability to create money and, as a result, lowering living standards.

When money is injected, it first enters a certain goods market. When the price of a good rises to the point where it is seen to be fully valued, the money moves to another market that is perceived to be undervalued. The transition from one market to another causes a time lag between monetary increases and their impact on the wealth generation process.

Central Banks Do Not Set Interest Rates. Individuals Do.

Note that contrary to popular thinking, interest rates are determined not by central bank monetary policy but by individual time preferences. According to the founder of the Austrian school of economics, Carl Menger, the phenomenon of interest is the outcome of the fact that individuals assign a greater importance to goods and services in the present versus identical goods and services in the future.

The higher valuation is not the result of capricious behavior, but rather that life in the future is impossible without sustaining it in the present. According to Menger:

Human life is a process in which the course of future development is always influenced by previous development. It is a process that cannot be continued once it has been interrupted, and that cannot be completely rehabilitated once it has become seriously disordered. A necessary prerequisite of our provision for the maintenance of our lives and for our development in future periods is a concern for the preceding periods of our lives. Setting aside the irregularities of economic activity, we can conclude that economizing men generally endeavor to ensure the satisfaction of needs of the immediate future first, and that only after this has been done, do they attempt to ensure the satisfaction of needs of more distant periods, in accordance with their remoteness in time.1

Goods and services essential to support one's existence now must be more important to that person than the same goods and services in the future. The person is more inclined to favor the same good in the now over the same good in the future.

Those with little resources can only contemplate relatively short-term aims, such as creating a simple tool. The small size of one's funds prevents him from undertaking the creation of more advanced tools. With more resources at his disposal, the individual may wish to try creating better tools. Individuals are able to dedicate more resources toward the achievement of distant goals in order to improve their quality of life over time as their pool of resources grows.

Prior to the development of means, the need to support life and wellbeing in the present made it impossible to undertake numerous long-term undertakings, but this becomes achievable with more resources at one's disposal.

Few, if any, people will engage on a company venture that offers a zero-percentage-of-return. The continuation of the process of life beyond hand-to-mouth subsistence necessitates an increase in money, and wealth increase indicates positive returns.

Are Lower Rates behind Increased Capital Goods Investment?

Contrary to popular belief, a decrease in interest rates does not lead to a rise in capital goods investment. The increase in the pool of savings, rather than the reduction in interest rates, allows for the expansion of capital goods.

People employed in the enhancement and extension of capital goods such as tools and machinery are supported by the pool of savings. It is possible to expand the production of future consumer products by increasing and improving capital goods.

Individual time preferences are signaled by allocating a considerably greater importance to future goods versus present goods when one decides to dedicate a greater amount of means to the production of capital goods. As a result, the interest rate reflects individuals' preferences about current consumption vs future consumption. (Once again, the drop in interest rates is not the source of the rise in capital investment. The reduction reflects the decision to allocate a larger amount of savings to capital goods investment).

In a free market, a drop in interest rates signals to firms that people favor future consumption products over present consumer goods. Businesses that want to succeed must follow consumer instructions and build a proper infrastructure to meet future demand for consumer goods. Individuals communicate increased savings by lowering their time preferences, which will encourage the expansion and improve the production structure.

Interest rate fluctuations in a free market will correspond to variations in consumers' timing preferences. As a result, a decrease in interest rates is caused by a decrease in consumers' time preferences. When firms see a drop in the market interest rate, they boost their investment in capital goods to accommodate the projected increase in demand for future consumer goods. (It is worth noting that in a free-market economy, a decrease in interest rates suggests that individuals have increased their preference for future consumer goods over present consumer goods.)

The central bank is responsible for the difference between the market interest rate and the interest rate that represents individuals' temporal preferences. For example, the central bank's aggressive loose monetary policy causes the observed interest rate to fall. Businesses respond to this decrease by boosting the production of capital goods in order to meet future demand for consumer goods. Consumers, on the other hand, have not demonstrated a shift in their preferences for current consumer items. Because the time preference interest rate did not fall, the spread between the time preference rate and the market rate widened.

Businesses responding to the dropping market interest rate have underinvested in capital goods relative to the production of current consumer products due to the gap between the time preference interest rate and the market interest rate. In the future, enterprises will learn that their previous capital goods expansion investment selections were incorrect.

Why Tightening Cannot Undo the Negatives of a Previous Loose Stance

According to Ludwig von Mises, a tight monetary stance cannot undo the negatives of the previous loose stance. (In other words, the central bank cannot generate a “soft landing” for the economy.) The misallocation of resources due to a loose monetary policy cannot be reversed by a tighter stance. According to Percy L. Greaves Jr. in the introduction to Mises's The Causes of the Economic Crisis, and Other Essays before and after the Great Depression:

Mises also refers to the fact that deflation can never repair the damage of a priori inflation. In his seminar, he often likened such a process to an auto driver who had run over a person and then tried to remedy the situation by backing over the victim in reverse. Inflation so scrambles the changes in wealth and income that it becomes impossible to undo the effects. Then too, deflationary manipulations of the quantity of money are just as destructive of market processes, guided by unhampered market prices, wage rates and interest rates, as are such inflationary manipulations of the quantity of money.

A tougher interest rate policy, while undercutting present financial bubbles, will also cause numerous distortions, causing wealth producers to suffer. A stricter posture is still central bank involvement, which distorts the interest rate signal. A tightening approach on interest rates does not result in the allocation of resources in accordance with consumers' top priorities. As a result, a tighter stance on interest rates does not imply that inflationary policy may be reversed. If we assume that inflation is caused by increases in the money supply, then all that is needed to eliminate inflation is to close the loopholes that allow the central bank to create money out of "thin air."

Price-stabilization policies, on the other hand, cause economic turbulence. Take note that by February 2021, the yearly growth rate of our monetary metric for the United States has risen to about 80%. Given the magnitude of the increase, it is not surprising that the CPI's annual growth rate has quickened. Policies aimed at decreasing the CPI growth rate rather than halting the increase rate of the money supply are likely to destabilize economic conditions.

Conclusion

Individuals will assign a larger price to present goods than future goods as long as life sustenance remains the ultimate aim, and no amount of central bank interest rate manipulation will change this. Any attempt by central bank policymakers to ignore this fact will jeopardize the process of wealth accumulation and degrade individual living standards. It will not aid economic growth if the central bank artificially lowers interest rates at a time when households have not saved enough to support the increase of capital goods investments. It is impossible to replace savings with additional money and to artificially lower interest rates because nothing can be created from nothing. The central bank cannot reverse the damage done by its past low interest rate policy by raising interest rates. Other distortions are likely to result from a tighter posture. As a result, policymakers should refrain from intervening in the economy.

=====

Related Video:

** Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of USA GAG nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.