More On: Inflation

Why Are We So Depressed?

Central bankers blame the victims in order to divide and rule

The chances that the Fed will cause the next bust are going up

A permanent economy based on war

The government will make you even poorer

Do the low inflation rates mean that the purchasing power of Japanese and Swiss citizens has increased relative to other countries over time? The answer seems to be no.

Japan and Switzerland have kept their interest rates lower than the U.S.'s interest rates since the early 1980s, even though the U.S.'s interest rates have been going down. Japanese government bonds have paid out about 2.8% less than U.S. government bonds have paid out since 1980. (see figure 1, left panel). The situation is the same in Switzerland (see figure 1, right panel), which is known as a safe place for international money. In both countries, the monetary policies have become more and more expansive. However, this hasn't led to high inflation because the huge increase in domestic money supply has only been partially absorbed by the domestic economy.

Figure 1: Ten-Year Government Bond Yields, Japan and Switzerland vs. the US

Source: Refinitiv.

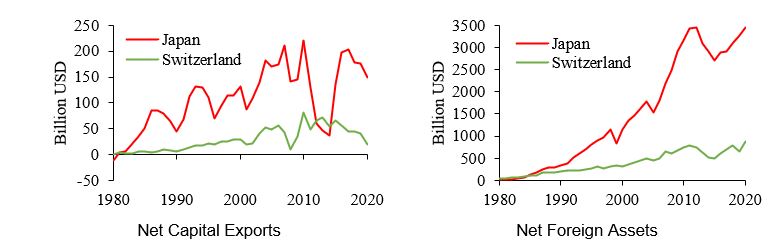

The low interest rates in Japan and Switzerland made it more difficult for foreign money to come in and more easy for money to go out. Since 1980, Japan's net capital outflows have on average been 2.5% of GDP per year. Switzerland's have been as high as 8.4% of GDP. The Swiss National Bank has been more involved in capital exports than the Bank of Japan. It has tried to keep the value of the franc from rising by buying euros (and selling francs). Capital has been leaving both countries for a long time, which has cut down on domestic price pressures. Products and homes in each country have both risen less quickly than they did in the United States.Second, low interest rates in Japan and Switzerland have led to an appreciation of the Japanese yen and the Swiss franc against the US dollar, on average by 1.4 percent (yen) and 1.0 percent (franc) per year since 1980. This is called open interest rate parity. Because Japan and Switzerland's net foreign assets have grown over time because of long-term outflows of money, both currencies are expected to rise in value (see figure 2, as well as McKinnon and Schnabl 2006 on Japan). If you look at the end of 2020, Japan's net foreign assets were $3.441 trillion, which is about 68% of GDP. Switzerland's were $867 billion (about 115 percent of GDP). If these foreign assets were repatriated, the yen and the Swiss franc would be under a lot of pressure to rise in value.

Figure 2: Japanese and Swiss Net Capital Exports and Net Foreign Assets

Source: International Monetary Fund.

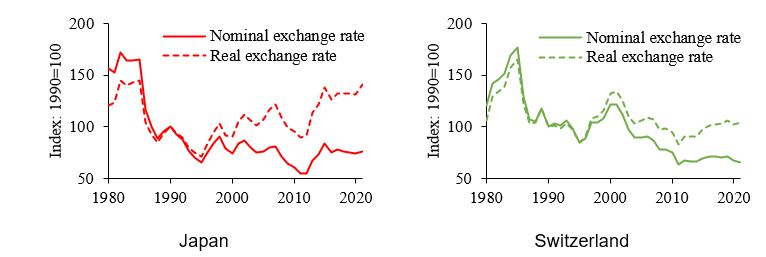

Third, there was a downward wage-price spiral because the appreciation pressure slowed growth and prices. Currency revaluations cut the prices of imported goods and made exported goods more expensive for people in other places. This made both Japanese and Swiss businesses that were interested in the market keep their prices low. To keep costs down, wage growth was held back. People in Japan and Switzerland may have been able to keep their wages down because their wages aren't as high as they are in other countries.However, Japan and Switzerland have strict wage and price policies compared to other countries, which has made the real exchange rate less valuable. This is the nominal exchange rate adjusted for changes in relative wages and prices. Japanese yen and Swiss franc real devaluation against the US dollar has averaged 1.4 percent and 0.7 percent per year since 1980 in terms of relative wage adjustment (0.7 percent and 0.4 percent per year in terms of relative price adjustment), which has hurt imports and helped exports. This has been bad for imports and good for exports. Japan and Switzerland have thus more than made up for the rise in the nominal exchange rate by having low wage and price growth than their foreign counterparts (see figure 3). This has cut domestic demand for foreign products and kept foreign demand for Swiss and Japanese products strong, which is why the two countries have always had big current account surpluses (see figure 2).

Figure 3: Nominal and Real Exchange Rates, Japanese Yen and Swiss Franc vs. US Dollar

Source: Organisation of Economic Co-operation and Development, Ministry of Health, Labour and Welfare (Japan), Federal Statistical Office (Switzerland), US Bureau of Labor Statistics. Note: The real exchange rate is adjusted for consumer price inflation. An increase (decrease) indicates a depreciation (appreciation) of the Japanese yen and Swiss franc against the US dollar.

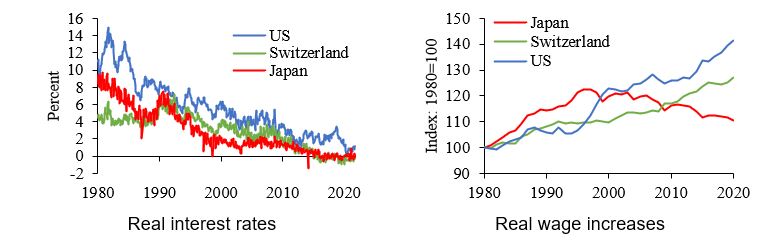

Over time, have the purchasing power of Japanese and Swiss citizens risen more than the purchasing power of people in other countries? Is the answer no? Because the real interest rate and real wage growth in both countries have been lower than in the United States, which is the most important market for Japanese and Swiss capital. Between Japan and Switzerland, the average real yield on ten-year government bonds since 1980 has been 2.9 percent. In the United States, it has been 5.5 percent (see figure 4, left graph).Because of this, the average real wage increase in Japan and Switzerland since 1980 is 0.3 percent. This is less than half of what it was in the United States, which saw an increase of 0.9 percent (see figure 4, right graph). From this point of view, people in Japan and Switzerland haven't really benefited from low consumer prices. Consumers in the US, on the other hand, seem to be getting more money to spend, which may be because of money coming from Japan and Switzerland.

Figure 4: Real Interest Rates and Real Wage Index in the US, Japan, and Switzerland

Source: Refinitiv, Ministry of Health, Labour and Welfare (Japan), Federal Statistical Office (Switzerland), and Social Security Administration (US).

References

Latsos, Sophia, and Gunther Schnabl. 2018. "Net Foreign Asset Positions and Appreciations Expectations on the Japanese Yen and the Swiss Franc." International Economics and Economic Policy 15(2): 261–80. https://doi.org/10.1007/s10368-017-0403-5.

McKinnon, Ronald, and Gunther Schnabl. 2006. "China’s Exchange Rate and International Adjustment in Wages, Prices, and Interest Rates: Japan Déjà Vu?" CESifo Economic Studies 52, no. 2 (June): 276–303. https://doi.org/10.1093/cesifo/ifl007.

=======

Related Video: