More On: recessions

What Americans Don’t Know about Inflation

Not Just Recession

There are two types of recessions, and the United States is likely to see one that is nothing like the one that occurred in 2008

The most likely reason why the average American has strange ideas about inflation is that they see inflation as the same thing as certain costs of living.

In exit polls after the midterm elections in the U.S., 31% of voters said that inflation was the "most important issue" that influenced their vote, which was the most of any factor listed.

But what do Americans really know about inflation, or what do they think they know?

The good news is that YouGov asked a lot of people about this question in the U.S. in late October. The bad news is that both the questions and the results showed a sad lack of basic economics knowledge.

Some Background

Before we look at why, let's first define inflation.Most textbooks would say that prices are going up all over the economy. Prices for goods and services on each market change all the time because of shocks in demand and supply. As more people move to Washington, DC to work at Amazon HQ, rents could go up. Because the price of gas at the wholesale level has gone up on the international market, energy bills may go up. Because of new laws that say childcare workers must have college degrees, there might be less care available, which could cause prices to go up. All of these could add to what people call their "cost of living." But this is not inflation by itself.

Instead, inflation is a large-scale economic event. It happens when there is too much money chasing the production of goods and services in the economy as a whole. This causes the overall price level to go up. The central bank, which in this case is the Federal Reserve, is to blame for inflation. We can't see "the aggregate price level," so we make price indices that measure how much the cost of a basket of typical goods that a consumer might buy has changed. In public debates, what happens to this Consumer Price Index is usually called "inflation," but it isn't a good way to measure the real issue that we care about, which is a big picture one.

So, in a way, all "inflation" is caused by bad macroeconomic policy. Assuming that the economy can produce goods and services, if central banks and governments work together through monetary and fiscal policy to let "too much money" chase a volume of goods, the price level will rise, pushing inflation above the central bank's target.

In reality, most economists would understand if central banks weren't able to predict exactly how productive the economy would be every year. So, if there is an unexpected "supply shock" that affects the whole economy, like the COVID-19 pandemic or high international wholesale gas prices because of the Ukraine war, or if the production of many goods suddenly slows down, measured inflation could temporarily go up for a given level of spending. In other words, it's not unreasonable to say that unusual supply-side factors and monetary incontinence can cause inflation, at least temporarily.

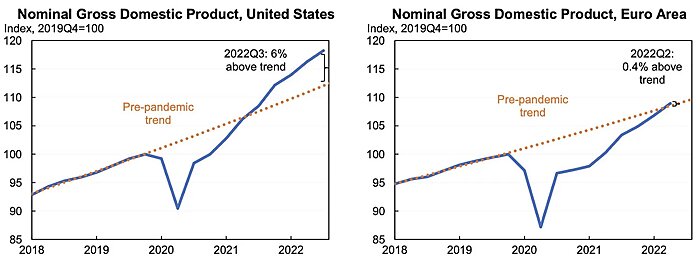

In fact, one reason why politics have been so hard during this time of rising prices is that both demand and supply factors have been at play at different times in the United States. Negative supply shocks, like the pandemic and the war in Ukraine, have hurt the economy and made the country less productive. Even though this is true, macroeconomic policy has been too loose compared to what was normal before the pandemic. This is shown by the fact that the growth of overall spending has been unstable.

As this chart below from Jason Furman shows, aggregate demand — the overall level of nominal spending in the economy — sped well above its pre‐pandemic trend from mid‐2021, meaning that macroeconomic policy was generating inflation, even if one generously says the Fed couldn’t have foreseen any impact of the supply‐shocks.

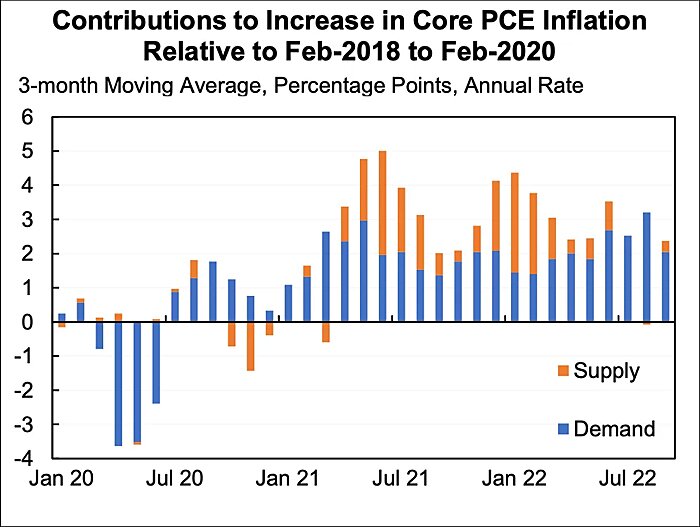

Though I’m skeptical that you can really do these types of studies given the complex interactions of prices, economists such as Adam Shapiro that have sought to decompose inflation into supply‐driven price increases and demand‐driven price increases have frequently estimated that “excess demand” is the key factor driving inflation today.

To YouGov polling…

Given what inflation is and isn’t, it’s deeply unhelpful that YouGov began its survey by asking Americans which goods and services they believed had increased in cost over the past 20 years. For this falls foul of conflating demand and supply changes for individual products over time (relative price changes) with later questions about the macroeconomic concept of inflation. And you soon see that the American public is indeed confused about all this.

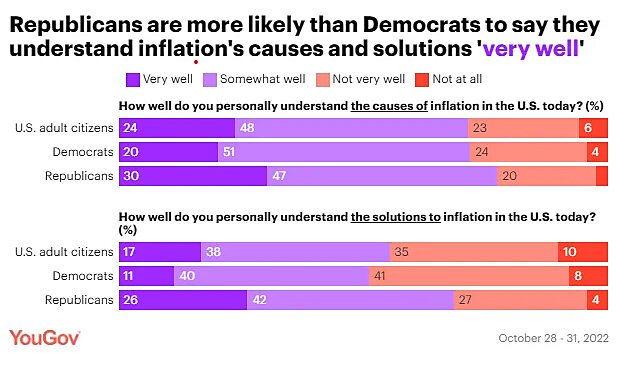

Their answers start reasonably enough: 72 percent of the public say they personally understand the causes of inflation “very well” or “somewhat well.” A far smaller proportion, 55 percent, say they understand the solutions to inflation well or somewhat well. This would be perfectly consistent with someone actually understanding inflation but displaying humility. There’s very few people in the world that understand the intricacies of the Federal Reserve’s operations, after all.

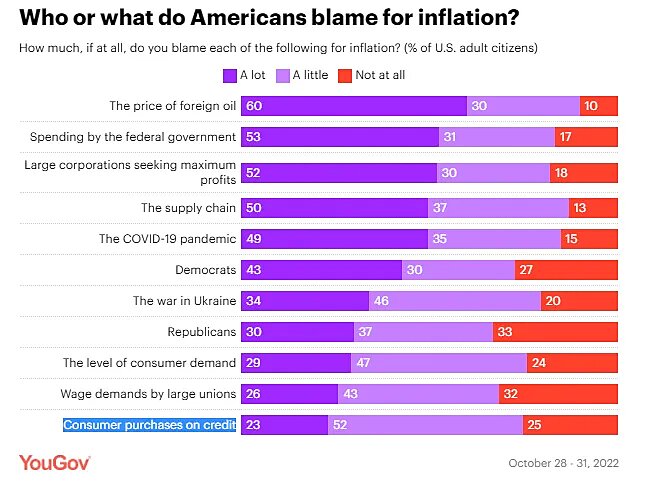

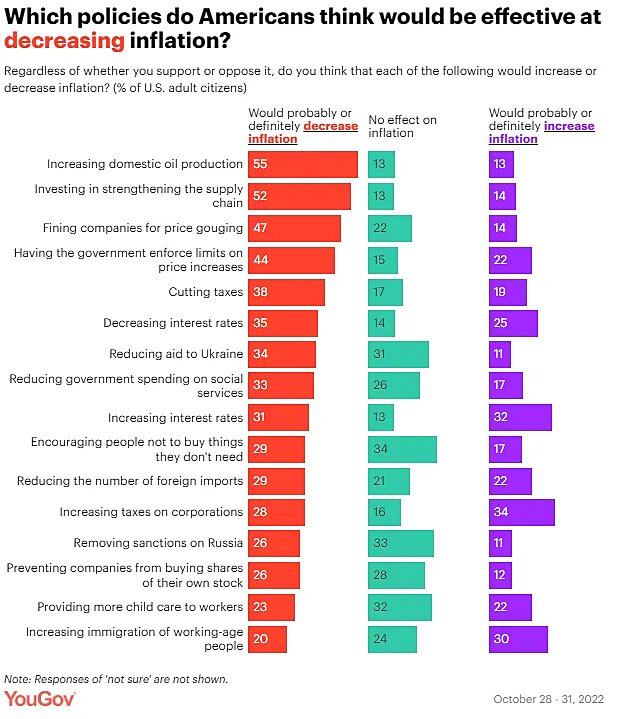

Alas, YouGov’s next question asked “How much, if at all, do you blame each of the following for inflation?” with 11 potential boogeymen listed (see below). The answers do not suggest that people’s understanding of inflation is well‐grounded.

The first problem is that “the Federal Reserve” was simply absent as an option for the public to pass judgment on. Whether it be interest rates being too low for too long, too much money in circulation, or any other monetary variable, YouGov simply didn’t give those surveyed the opportunity to blame monetary policy and the Federal Reserve at all for today’s inflation. That is a massive oversight.

Of the options they were given, there were some reasonable responses:

-

a huge 90 percent of Americans blamed “the price of foreign oil” a lot (60 percent) or a bit (30 percent) for today’s inflation, which, as a contributor through its supply‐side impact, is fair enough.

-

81 percent blamed too much federal spending. Given government institutions printed and borrowed trillions and sent people checks that compensated them far beyond necessary for income‐smoothing during the pandemic, this has a strong grounding in several macro theories for increasing the price level too.

-

84 percent blamed the “COVID-19 pandemic.” This, again, is reasonable given both the hit to supply the pandemic caused and the huge macroeconomic stimulus that was generated in response to it.

For example, a huge 82 percent of the public thinks that inflation can be blamed on "large corporations trying to make as much money as possible." Still, corporations always want to make money. Profitability can only go up at the same time as inflation if overall spending is going up faster than output. This drives up prices first while wages stay the same, which increases profit margins. In fact, if one company tried to raise prices without doing this, they would either lose customers or their customers would have less money left over to buy other things, which would lower demand and therefore prices elsewhere. So, greedy companies can't cause "inflation," since it's almost always caused by too much spending as a whole.

For the same reasons, the 69 percent of people who think inflation is caused by "wage demands by large unions" are also wrong. As the price of labor goes up, nominal wages will go up sharply during an inflationary period, and many manufacturers and retailers will find that they have to raise their prices to cover their rising (or expected) costs. But this doesn't mean that rising wages are the main reason why prices are going up. If a union is aggressive and tries to raise wages without increasing the amount of money available to spend, and producers try to pass on these costs by raising prices, most of them will just sell less. Again, this will lead to less work being done and fewer jobs. Higher costs can only be passed on to customers in the form of higher prices if customers have enough money to pay the higher prices. Again, there must be too much money in the economy as the ultimate cause of inflation in the whole economy.

The blame game turns to policy

Perhaps unsurprisingly, dodgy views on who is to blame for inflation feeds through into whacky ideas for “solutions” for dealing with it:

-

47 percent and 44 percent of Americans believe anti‐price gouging laws and direct government price controls would be effective at decreasing inflation, respectively.

Yet banning or deterring individual price increases will lead to shortages of those products, bottlenecks and a waterbed effect whereby uncontrolled prices increase for a given level of spending. Economy‐wide price controls would be a disaster too — with historic experience showing businesses allowing product quality to deteriorate or shrinkflation to occur to reflect the controlled prices, or else a sharp rebound in prices to their true level when controls are lifted.

-

Many more Americans believe cutting taxes and reducing interest rates will reduce inflation than increase it.

I doubt this is because they hold complex views that targeted tax cuts could boost aggregate supply substantially or because they are neo‐Fisherians on monetary policy either. What this suggests to me is that people associate “inflation” with the cost of living generally, rather than see it as a consequence of expansionary macroeconomic policy. Since paying taxes and mortgage costs are also living costs for many people, they think lowering taxes or reducing interest rates would ease the squeeze on them and so see these policies as disinflationary.

-

More Americans believe “reducing the number of foreign imports would decrease inflation” than increase it.

While protectionism would only have the direct effect of raising the relative price of those goods protected (not inflation), doing more of it would make the economy overall less productive. If anything this would slightly raise the prospects for temporary inflation for a given level of spending.

-

A net 10 percent of Americans believe that “increasing immigration of working‐age people” would increase inflation.

Again, the impact of immigration would primarily alter relative prices. The net impacts of more immigration are complex because more workers would boost the supply of goods, but their spending boosts demand too. I suspect Americans take the position that more migration would raise inflation because they envisage things like higher house prices — again, conflating “inflation” with the cost of living of essential goods.

Where do these views come from?

The best explanation for why the median American holds quirky views on inflation is that they see inflation itself as synonymous with certain day‐to‐day living expenses. So, anything that they think might reduce their major out‐of‐pocket expenses — lower taxes, lower mortgage rates, less greedy companies, less greedy unions — is deemed good for reducing inflation too.

The question then becomes: where does this misguided understanding of inflation come from?

Part of the problem, no doubt, is just a lack of basic economic literacy — not just among the public, but in the broader debates around inflation that the public hear. One reason that I started writing The War on Prices is because I could see that this inflationary moment was leading to all sorts of bad ideas resurfacing, whether theoretical (wage‐price spirals) or policy‐based responses (price controls). The fact that YouGov didn’t even include the Federal Reserve as a source of blame for inflation speaks volumes. The conflation of inflation with individual price changes is also pervasive.

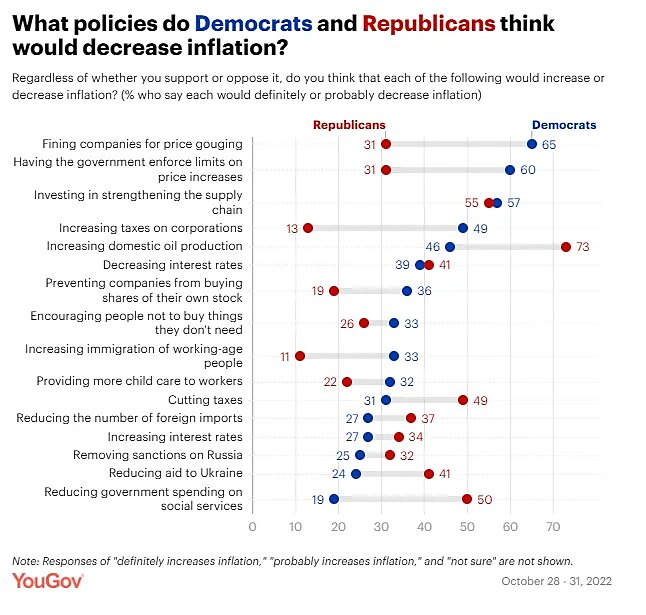

And, to be honest, it's not always a bad thing from a policy point of view when some of these theoretical differences between relative price changes and inflation start to blur. High inflation can lead to bad things like price controls and smear campaigns against businesses, but it can also lead to good things like the deregulation of important industries during the Carter-Reagan era. If the U.S. got rid of supply-side restrictions on new energy production right now, it could have the same good effects.But it's hard to look at the results by party and not think that there is either a top-down absorption of political narratives by party or that people tell pollsters what they think a Republican or Democrat loyalist would say.

Most likely, Democrats will say that corporations, the pandemic, supply chains, and Republicans are to blame for inflation. Most of the time, Republicans will blame federal spending, Democrats, and the price of oil in other countries. When you think about how long each party was in charge of the U.S. Presidency, it's clear that both of these sets of explanations are useful for shifting blame.

And the blame game has an effect on how policy is made. Democrats think that the best ways to stop inflation are to control prices, put money into supply chains, and tax corporations. Republicans say it increases oil production in the United States, cuts taxes, and cuts government spending. Even though not all elected politicians from either party would agree with these suggestions, they are mostly in line with what prominent Dems and GOP members have said about their policies or what they are upset about.

Americans and pollsters, then, have rather misguided opinions on what inflation is and what caused it this time. At least part of this seems to just be a folksy conflation between inflation and certain important product prices. Add to that the way that everything in the U.S. has become politicized and it’s clear that, except for the role of Vladimir Putin, there’s little shared economic narrative among American voters about inflation or how to deal with it.

Other Things

-

My Times column this week argued that if the Tories were serious about a fiscal framework to restrain debt, they should look to Switzerland, where it has actually worked.

-

Several states and DC are chasing the price level with aggressive minimum wage hikes (ugh).

That’s all for now!